American workers with 401(k) plans are right to dread a stock market crash that would wipe out a big chunk of their hard-earned balances.

But instead of living in fear, it's possible to do something about it - thanks to the option of money market funds, which almost every 401(k) plan offers.

A lot of people don't realize how easy it is to make the changes to their 401(k) that would protect them from a market collapse. Only one in six 401(k) participants ever change the investments in their plan, according to U.S. News. Either they don't believe they are allowed to rebalance, or they don't know how.

Moreover, many investors wrongly believe their 401(k) assets are required to stay invested in the markets, no matter what the structural risks are. They've heard about the onerous tax penalties and fees associated with "early withdrawal," so they don't touch them at all.

So every time there's a major market downturn, they lose.

Most importantly, they don't know that moving into a money market fund will protect those assets from a market crash.

But it doesn't have to be that way.

Money Market Funds Provide Market Crash Protection

The best way to protect your 401(k) balance from a market crash is to re-allocate some of your money into one of the money market fund investment options. Most 401(k) plans offer at least one such option.

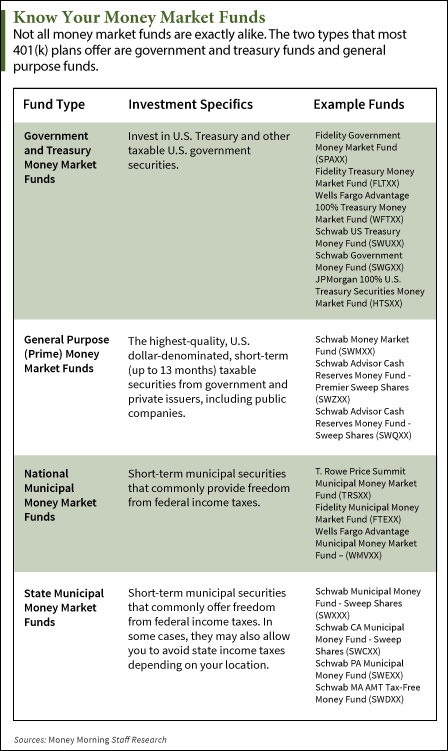

Money market funds are simply mutual funds that invest in short-term (less than one year) securities representing high-quality, liquid debt and monetary instruments. These often include short-term government securities, companies, and repurchase agreements.

In most cases the goal is to maintain a net asset value (NAV) of $1 per share while offering a modest return.

Click to Enlarge |

In many ways, they're like a savings account - a safe and accessible place to store your cash, but better.

You see, money market funds pay much higher "interest."

The average savings account interest rate is a dismal 0.06%, according to the FDIC (as of September 2014).

Most money market funds beat that handily, yielding usually 0.01% every seven days, or 0.52% annually, thanks to the structure of the bonds.

Money market funds are extremely low-risk, too. In fact, there are rules that automatically reduce risk. No investment in the fund can exceed 13 months in duration, and the average weighted maturity in the portfolio is 60 days or less. And these funds are not subject to market timing considerations; you can buy and sell them at any time.

And of course the most important thing is that because they're not invested in equities, money market funds don't lose value in a stock market crash.

Here's how to get started:

What You Need to Know About 401(k) Money Market Funds

First of all, be very clear that we are not talking about withdrawing money from a 401(k) to invest in a money market fund. That would be a very unwise move, as withdrawing from your 401(k) early - before the age of 59½ - or redirecting funds elsewhere can lead to an early withdrawal penalty as high as 10%, new fees, and could push your tax return into a higher income bracket.

At the same time, you could elect to shift a portion of your investments outside of your 401(k) - at a brokerage for example - to a money market account. (Brokerages commonly keep clients' cash in money market accounts anyway.)

As for how much of your 401(k) you might want to transfer to a money market fund, that's going to vary by individual. A good ballpark to start with is to have about 20% of your holdings in some form of cash, which can include money market funds. If you're not sure what proportion is right for you, consult a financial advisor.

To give you some idea of what the reallocation process will look like and how to go about it, we contacted some of the biggest and most reputable 401(k) administrators: T. Rowe Price, Vanguard, Fidelity, and Wells Fargo.

Here's what we learned:

- Contact your 401(k) plan representative and ask about rebalancing or changing your investments. You can find the contact information on your most recent 401(k) statement or on your plan administrator's website.

- Find out which money market funds you can choose from. The ones that are available to you through your 401(k) will vary based your plan administrator. Ask about the differences. Find out if any have a minimum investment, as well as about the yield and fees. You can request a prospectus for the ones you choose.

- Decide which investments to drop. In general, the money going into a money market fund should come from index funds that will tank right along with the broader market. In particular, the sectors that will take the biggest hit during a crash are highly leveraged financial stocks, U.S. retail and housing, consumer discretionary, U.S. auto companies, travel and leisure stocks, and companies that depend on radio and online ad revenues.

- Ask about taxes and fees. Gather as much information as you can about taxes related to capital gains on the investments you sell. Also find out about possible fees tied to reallocating any of your 401(k) assets into a money market fund. Most are unlikely to charge fees, but there could be charges that you will want to know about before acting.

- Reallocating your 401(k) balance: Most plan administrators will let you make this request over the phone, in person or online. If you want to make changes to your 401(k) online, you will need to have (or create) a user name and password for your account. A note on timing: Some plans will allow you to rebalance your 401(k) whenever you want, but some restrict how frequently you can make changes. Current federal guidelines suggest plans allow their participants to rebalance or select new investments at least once a quarter, but it's not a law.

- Reallocating your contributions: Changes made to your balance do not affect the allocations of future contributions. (This does not affect folks no longer making contributions.) If you want the same proportion of future contributions to go into the money market fund where you've reallocated part of your balance, you need to take that action separately.

- Get confirmation. After the transaction is complete, you will receive a confirmation number and message. It is vital that you keep this for your records to ensure that the transaction has been completed. Following this confirmation, it is very common for trades to be completed within 24 hours, but it may take as long as three days. Check your next statement to verify that your reallocation has taken place.

One Last Thing: Know the Risks

While keeping some 401(k) assets in money market accounts can save you from huge losses in a market crash, the strategy isn't without some trade-offs - which is why you should discuss any moves beforehand with a qualified financial advisor.

Keep these points in mind:

- There are opportunity costs of being out of the market altogether. Although the economy carries significant structural risks, fueled by ongoing stimulus efforts and unsustainable debt levels, the markets could continue to rise in the months ahead. It's unclear exactly which "flashpoint" will set off the eventual crisis - and when.

- Second, there are major risks to the U.S. dollar. A number of governments continue to raise concerns about the health and stability of the U.S. dollar. Given the U.S. Treasury Department's ability to print dollars, it is unlikely that the U.S. will default on its debts. However, the threat of inflation is a constant in any high-debt society, particularly as a government seeks to eradicate its obligations.

- Finally, money market funds did experience concerns in the wake of the financial crisis in 2008. It wasn't the exposure to short-term U.S. government securities or other municipal debts, but the "prime" funds, with exposure to short-term corporate debt, that sent shockwaves through the markets. Back on Sept. 16, 2008, a huge money-market fund, the Reserve Primary Fund, announced that its net asset value (NAV) slipped below the $1 level, to $0.97. Known as "breaking the buck," this type of incident is rare; the 2008 episode was the first time it had happened in 14 years.

UP NEXT: The U.S. Treasury is planning to introduce a new type of retirement savings account, the myRA, within the next few months. Though billed as a new way to help Americans build up a retirement nest egg, the reality is something else entirely. Here's why you should avoid opening a myRA account...

[epom]