By Lee Adler

Weak corporate tax collections in the first quarter and through April 11 could mean that many quarterly earnings reports may surprise the market by failing to meet analysts' inflated expectations. Either corporate profits are falling sharply or else corporations have suddenly become much savvier about offshoring income and avoiding taxes. While they may be getting better at avoiding taxes, it seems unlikely that they've suddenly all become such geniuses at it simultaneously. My bet would be that when everybody has reported, aggregate earnings will fall short of consensus estimates.

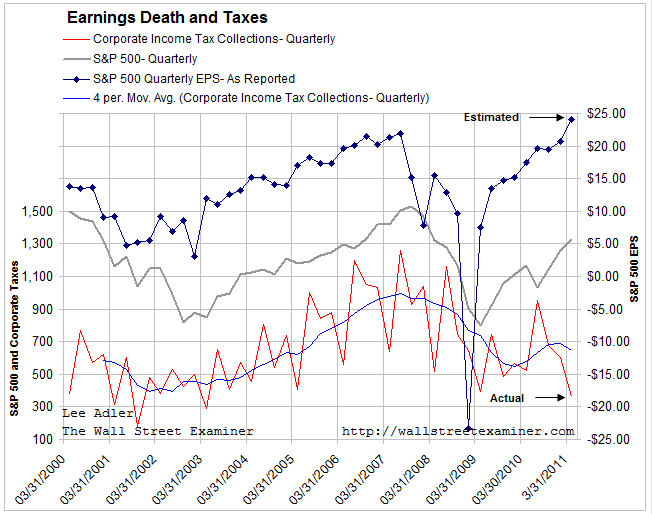

The Treasury Department publishes daily data on tax collections. As of 5 PM each weekday it releases the Daily Treasury Statement for the previous day. That's as close as we can get to a real time economic barometer short of being at the cash register. It's definitely useful in gauging whether subsequent corporate earnings reports will meet, beat, or miss expectations. Corporate tax collections and subsequent reported aggregate earnings have correlated well historically, not just in terms of the trend, but even to the extent that the peaks and valleys in tax collections are echoed at lower amplitude in the earnings line.

The government collected $36.1 billion in corporate taxes in the first quarter. That includes the taxes due on March 15 for the prior calendar year. That number is down 31% from collections in Q1 of 2010. Collections since then through April 11 suggest a continuation of that weakening trend for the first quarter. The final final verdict on the quarter will not be in until April 18, the date that quarterly taxes are due this year. While, it's theoretically possible that the numbers could recover when the final tally is in for April 18, the indications for the period so far continue to point down.

Standard and Poors estimated that first quarter earnings on the S&P 500 would be up 38% year over year. How can income tax collections be down? These two numbers should not be going in opposite directions. One of them is actual, and one of them represents analysts' estimates. We know that analysts can be wrong. Could they be that wrong?

Admittedly the two numbers don't represent the same thing. Earnings are worldwide. Federal taxes are only due on income earned in the US. But still, these numbers should correlate, and over the past 9 years they have usually correlated well. The fact that they are now headed in opposite directions should get our antennae up.

Contrary to popular belief, stock prices trail earnings, not vice versa. And earnings clearly track with tax collections. The last time we saw a big negative divergence between taxes versus earnings and stock prices was in the summer of 2007, when tax collections began to turn down ahead of earnings and stock prices. An upside reversal in tax collections also led the turn to a bull market in 2003. They were late at the 2009 low, but that was because Congress, in its infinite wisdom, granted tax relief to a wide swath of the business world.

The fact that these indications were available in real time, ahead of the earnings reports, gave anyone who was paying attention a nice heads up on the bear market in 2007. The current divergence is significantly bigger than that one.

So is this a case of corporations suffering a big earnings decline in Q1, or is it a case of them suddenly getting better at avoding taxes? If it's the former, investors are in for a shock. The market is expecting much higher earnings, which tax collections suggest have not materialized. If it's the latter, it brings to mind that US corporations have all the rights of individuals but less of the responsibilities, like paying taxes. Since the Supreme Court has ruled that they can secretly spend as much as they want to influence tax policy, it might be good for the US stock market, but it's bad for the American people. Just something to keep in mind, if in fact earnings report meet expectations.

Having seen this data my bet would be that they miss in a big way. Maybe the market's reaction to Alcoa's earnings is the first glimmer of recognition of what the tax data has been telling us.