Taking a header off the "fiscal cliff" might be the best thing that could happen to the United States.

It sounds crazy, given all the dire predictions economists are making about the "Taxmageddon" that will arrive on Jan. 1, 2013.

While true, no one is talking about what would happen to the economy after the fiscal cliff crisis of 2013.

If Congress fails to act and allows all the bad things to happen - the expiration of the Bush-era tax cuts and the payroll tax cut, as well as the enforced spending cuts (sequestration) agreed to in the budget deal last year - the federal budget deficit would start shrinking dramatically.

And the fiscal discipline, while brutal in the short run, would jump-start the economy by early 2014.

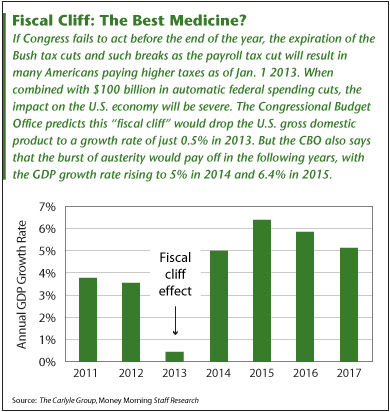

It's all in a recent Congressional Budget Office (CBO) report, "Economic Effects of Reducing the Fiscal Restraint That Is Scheduled to Occur in 2013."

The CBO ran projections based on two scenarios.

One looks at what would happen if Congress does nothing and lets the country go over the fiscal cliff. The other scenario looks at what would happen if Congress dodges the fiscal cliff by extending most, if not all, of the current policies.

Choosing to take a leap off of the fiscal cliff--as has been widely reported-- would slam an already faltering U.S. economy. The CBO report says GDP would shrink by 1.3% in the first half of 2013, pushing the country back into a recession.

On the other hand, extending current policies would push GDP up 5.3% in the first half of 2013.

That may sound great, but a funny thing happens after those first six months.

In the CBO's fiscal cliff scenario, GDP turns the corner in the second half of 2013, rising 2.3%. Then, in 2014, GDP jumps up 5%, followed by an astounding 6.4% increase in 2015.

The initial growth spurred by extending current policies, however, starts to peter out after six months. By the second half of 2013, the CBO says GDP would slow to 3.4%. From there, slower growth would continue through 2016.

"Postponing the fiscal cliff would simply move economic activity from 2014-2016 into 2013," say Jason M. Thomas and David M. Marchick in a May 31 report for the Carlyle Group. "The result would be faster growth in 2013, slower growth between 2014 and 2016, and no change in cumulative growth rates over the next four years."

The Cost of Ducking the Fiscal Cliff

Given that avoiding the fiscal cliff only borrows a little growth from future years, at first blush it looks like a winner. But its impact on the national debt would cripple future economic growth.

The CBO looked at that, too.

Extending the policies of tax cuts and high government spending would drastically accelerate the national debt. The CBO says federal debt held by the public, about 73% of GDP as of this year, would rise to 93% by 2022 and about 200% by 2037.

But if America plunges off the fiscal cliff, the debt held by the public declines to 61% in 2022 and just 53% in 2037.

Those who believe debt doesn't matter much may dismiss this fact, but the CBO also projected how the ballooning debt would increasingly stunt economic growth in the decades ahead.

"Large budget deficits would reduce national savings, thereby curtailing investment in productive capital and diminishing future output and income," the CBO report says.

Policies that avoid the fiscal cliff would reduce GDP 1.8 percentage points by2027 and 6.7 percentage points by 2037.

The CBO's numbers for the gross national product (GNP) look even worse. GNP differs from GDP in that it includes the flow of profits and interest both to and from foreign countries.

According to the CBO, the rising debt will cause more foreign capital to enter the United States, which will eventually lead to higher payments of profits and interest to foreigners.

Extending current policies would take 4.4 percentage points out of the GNP by 2027 and a startling 13.5 percentage points by 2037.

The CBO warns: "Debt cannot continually increase as a share of the economy: Policy changes would be required at some point. The longer the necessary adjustments in policies were delayed, and the more that debt increased, the greater would be the negative consequences."

Congress Must Face the Fiscal Cliff

Which path the country takes is mostly in the hands of Congress.

The CBO recommends that lawmakers take a middle road that softens the blow to the economy in 2013 while still addressing the long-term debt issues that would undermine the economy.

But that will require bipartisan cooperation, a commodity in short supply on Capitol Hill.

"I will again insist on my simple principle of cuts and reforms greater than the debt limit increase," Speaker John Boehner, R-OH, said last month at a fiscal summit sponsored by the Peter G. Peterson Foundation. "This is the only avenue I see right now to force the elected leadership of this country to solve our structural fiscal imbalance."

That statement elicited this response:

"I would far prefer to see these issues resolved sooner rather than later, but it's hard to be hopeful about that in light of comments by Speaker Boehner," Rep. Chris Van Hollen, D-MD, ranking member of the House Budget Committee, told Politico. "Instead of talking about coming together and finding common ground, he is laying down reckless economic ultimatums."

It sounds like another round of gridlock, but this time the stakes are much higher. Last year's debt ceiling battle cost the United States its AAA credit rating.

Whatever Congress does -- or doesn't do -- about the fiscal cliff before Dec. 31 will have much more far-reaching consequences.

"We don't know how to price the risk of the fiscal cliff, particularly after last year," Jerry Webman, chief economist at Oppenheimer Funds, told Politico. "And if last year they [Congress] were playing with matches, now they're playing with flamethrowers."

Related Articles and News:

- Money Morning:

Are You Ready for "Taxmageddon"? - Money Morning:

Romneynomics: What You Can Expect if Mitt Romney Wins the Election - Money Morning:

Obamanomics: What You Can Expect if President Obama Wins the Election - Congressional Budget Office:

Economic Effects of Reducing the Fiscal Restraint That Is Scheduled to Occur in 2013 - Congressional Budget Office:

The 2012 Long-Term Budget Outlook - FactCheck.org:

GDP vs. GNP - CNN Money:

CBO: Hard choices ahead on debt - Washington Post:

Boehner: Watch out for that fiscal cliff

About the Author

David Zeiler, Associate Editor for Money Morning at Money Map Press, has been a journalist for more than 35 years, including 18 spent at The Baltimore Sun. He has worked as a writer, editor, and page designer at different times in his career. He's interviewed a number of well-known personalities - ranging from punk rock icon Joey Ramone to Apple Inc. co-founder Steve Wozniak.

Over the course of his journalistic career, Dave has covered many diverse subjects. Since arriving at Money Morning in 2011, he has focused primarily on technology. He's an expert on both Apple and cryptocurrencies. He started writing about Apple for The Sun in the mid-1990s, and had an Apple blog on The Sun's web site from 2007-2009. Dave's been writing about Bitcoin since 2011 - long before most people had even heard of it. He even mined it for a short time.

Dave has a BA in English and Mass Communications from Loyola University Maryland.