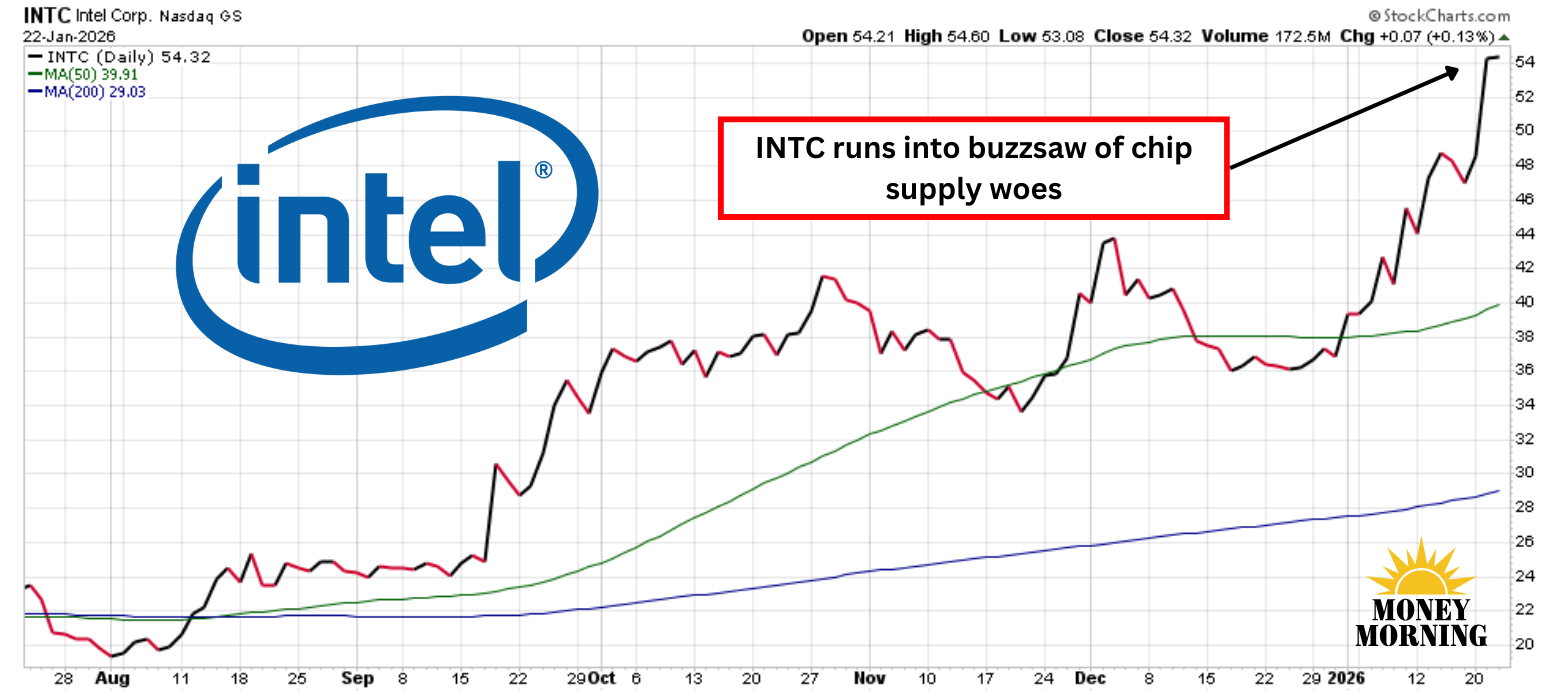

Intel Plunges After Offering Weak Guidance. Should You Buy the Dip?[Featured](https://moneymorning.com/category/featured/) # Intel Plunges After Offering Weak Guidance. Should You Buy the Dip?  by Rich Duprey  January 23, 2026  Share it: **Intel** ( [INTC](https://moneymorning.com/stocks/intc/)) delivered a robust finish to its fiscal 2025 with fourth-quarter earnings released after the bell on January 22, 2026. The chip giant posted revenue of $13.7 billion, topping Wall Street's consensus estimate of $13.41 billion despite a 4% year-over-year dip. Adjusted earnings per share came in at $0.15, smashing expectations of $0.08 and marking a significant improvement from the prior year. However, investor enthusiasm quickly soured as Intel's forward-looking statements painted a cautious picture. The company forecasted first-quarter revenue between $11.7 billion and $12.7 billion – the midpoint of $12.2 billion fell short of the $12.55 billion expected – and breakeven adjusted EPS against hopes for $0.05. Citing severe chip supply bottlenecks peaking in Q1 before easing in Q2 and beyond, shares are tumbling 14% in premarket trading this morning, erasing much of the recent rally and pushing the stock down to around $47 from its close above $54 per share.  ## Q4 Highlights and Gloomy Guidance Diving deeper, Intel's Q4 success stemmed from resilient demand in key segments. Data Center and AI revenue climbed 9% year-over-year to $4.7 billion, fueled by strong AI infrastructure expansion, hyperscaler needs, and the enduring appeal of the x86 ecosystem. Custom ASICs saw growth exceeding 50%, reaching an annualized run-rate over $1 billion. Overall, the quarter marked Intel's fifth straight beat on guidance, with non-GAAP gross margins at 37.9% (140 basis points above prior guidance), bolstered by disciplined spending, lower inventory reserves, and positive free cash flow of $2.22 billion – a sharp turnaround from the prior year's negative figure. Yet, the spotlight shifted to Intel's supply woes. CFO David Zinsner explained that industry-wide shortages, combined with Intel's internal production ramps for advanced nodes like Intel 18A, would constrain output the most in Q1. The company is prioritizing wafer allocation to higher-margin server and AI products over seasonal PC demand in the Client Computing Group, leading to a more pronounced revenue decline there. CEO Lip-Bu Tan stressed aggressive efforts to scale supply for new AI-focused chips like Panther Lake, assuring meaningful improvements from Q2 onward amid healthy underlying demand across markets. ## Valuation in the Wake of Pre-Earnings Hype Leading into earnings, Intel's stock surged nearly 50% in 2026, propelled by a flurry of analyst upgrades from firms highlighting sold-out server CPU capacity for the year, AI demand tailwinds, foundry progress (with 18A yields steadily climbing toward commercial viability), and strategic bets like potential external customer commitments. This optimism drove shares to multi-year highs above $54, inflating valuations, with a market cap around $230 billion and a price-to-sales ratio exceeding 4. That multiple appears steep for a company still navigating thin profitability, GAAP losses, and sequential revenue declines ahead. Trailing P/E ratios remain elevated due to compressed earnings, while average analyst price targets hovered around $41 to $45 before the earnings report, signaling overvaluation and slim margin for error if execution slips further amid persistent supply hurdles. ## Bottom Line Despite the lofty pre-earnings valuation, Intel is advancing its turnaround under refreshed leadership, with promising traction in AI and data center growth, 18A node ramps, and foundry momentum – albeit with timelines slipping due to yield and capacity challenges. This plunge might tempt investors to buy the dip seeking exposure to AI and domestic manufacturing themes, but caution is still warranted. Guidance for Q2 will be pivotal, revealing whether management's view of this as a temporary supply hiccup – with demand intact and margins and chip availability improving – holds true, or if deeper issues derail the recovery. **Beat the market, without relying on brokers or biased institutions.** Email(Required) URL This field is for validation purposes and should be left unchanged. Subscribe By submitting your email address, you will receive a free subscription to _Money Morning!_ and occasional special offers from us and our affiliates. You can unsubscribe at any time and we encourage you to read more about our [Privacy Policy](https://moneymorning.com/privacy/). ## One moment, please: Processing your submission ###### More Trending Stories from Money Morning - [Here's Why ACM Research Is a Buy Despite Its Earnings Miss](https://moneymorning.com/2026/03/01/why-acm-research-is-a-buy-despite-earnings/) - [$10,000 Invested in MercadoLibre 5 Years Ago Would Be How Much?!](https://moneymorning.com/2026/02/27/10000-invested-in-mercadolibre-5-years-ago-would-be-how-much/) - [Is a Buyout the Hope PayPal Investors Have Been Waiting For?](https://moneymorning.com/2026/02/27/is-a-buyout-the-hope-paypal-investors-have-been-waiting-for/) - [Here's Why ACM Research Is a Buy Despite Its Earnings Miss](https://moneymorning.com/2026/02/27/heres-why-acm-research-is-a-buy-despite-earnings/) - [Axon Enterprise Stuns the Market With Huge Q4 Earnings Beat](https://moneymorning.com/2026/02/27/axon-enterprise-stuns-the-market-with-huge-q4-earnings-beat/) Share it: ### Popular Articles ###### [Is a Buyout the Hope PayPal Investors Have Been Waiting For?](https://moneymorning.com/2026/02/27/is-a-buyout-the-hope-paypal-investors-have-been-waiting-for/) February 27, 2026 ###### [Anthropic Mauls CrowdStrike Again. Here's Why the Cybersecurity Stock Is a Buy](https://moneymorning.com/2026/02/25/anthropic-mauls-crowdstrike-again-heres-why-the-cybersecurity-stock-is-a-buy/) February 25, 2026 ###### [Nvidia's Deal With Meta Is Ringing Alarm Bells at Intel and AMD](https://moneymorning.com/2026/02/23/nvidias-deal-with-meta-is-ringing-alarm-bells-at-intel-and-amd/) February 23, 2026 ###### [Carvana Posts Record Q4 Results, But the Stock Is Still Not a Buy](https://moneymorning.com/2026/02/20/carvana-posts-record-q4-results-but-the-stock-is-still-not-a-buy/) February 20, 2026 Notifications reCAPTCHA Recaptcha requires verification. [Privacy](https://www.google.com/intl/en/policies/privacy/) \- [Terms](https://www.google.com/intl/en/policies/terms/) protected by **reCAPTCHA** [Privacy](https://www.google.com/intl/en/policies/privacy/) \- [Terms](https://www.google.com/intl/en/policies/terms/)