If you are looking for a steady stream of safe dividends in today's troubled markets, the list of "Dividend Aristocrats" is a good place to start.

Compiled and tracked by Standard & Poor's, Dividend Aristocrats are companies that have consistently increased their dividend payouts for 25 consecutive years.

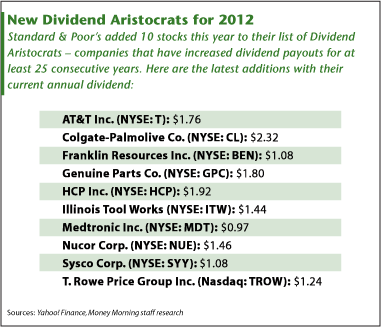

Currently, there are 51 of them, including the 10 new Dividend Aristocrats added this year.

That offers yield conscious investors a choice of 51 solid companies with a reliable track record of providing guaranteed payments-even during volatile markets and down economic cycles.

"The problem with going for capital growth is that you very often don't get it, and then you've got nothing – the investment just sits there," said Money Morning Global Investing Specialist Martin Hutchinson.

"Dividends" Martin says, "are easy."

Not only are they easy, they're also increasing.

Dividends on the Rise in 2012

Standard & Poor's reported that dividend increases for all their indices in 2011 almost doubled the dividends paid in 2010.

Total dividend increases hit $50.2 billion last year – an 89.2% rise over 2010's dividend increases of $26.5 billion – and are expected to climb even higher in 2012.

That's welcome news for investors searching for steady income sources in a zero-growth environment.

Few other assets – especially bonds – are expected to deliver an increased payout this year.

"With 10-year Treasury bond yields below 2%, bonds just don't give you the income they used to," said Hutchinson. "Dividend stocks can give you a better yield than bonds, and if you pick the right ones, will provide both protection against inflation and a chance to share in global economic growth. While they'll fluctuate with the market, dividend stocks of attractive companies are thus really a three-fer."

Dividend Aristocrats even go a step further than ordinary dividend stocks because of their lengthy payout history.

But before you dive into investing in these Dividend Aristocrats, the list needs some scrutiny.

But before you dive into investing in these Dividend Aristocrats, the list needs some scrutiny.

Even though all 51 Aristocrats are known for increasing dividends, not all of them make for great investments in today's market.

"All you have to do is figure out which companies are run by sharpies – and are paying dividends out of capital – and which companies have genuinely solid business models that aren't going away," said Hutchinson.

In fact, there's only one of the freshly-minted Aristocrats that you should add to your portfolio right now.