Debt is the proverbial double-edged sword, offering access to costly assets, but sometimes driving overleveraged borrowers into bankruptcy.

Only politicians and some Keynesian economists could convince themselves - along with a good portion of the masses - that more debt is the solution to the world's already crushing levels.

It's gotten so backwards, it's downright scary.

Yet there are some practical things you can do to avoid getting sucked under by the growing sea of debt.

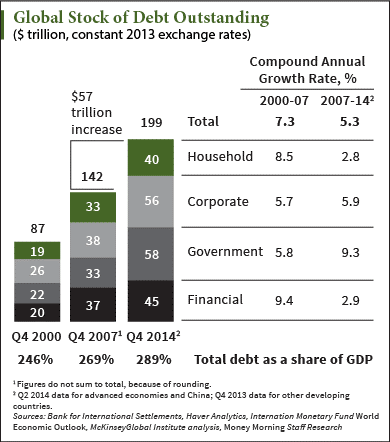

According to a study recently published by the McKinsey Global Institute, a research and consulting firm, worldwide debt levels have exploded. Although common sense had many expecting that world economies would deleverage after the Financial Crisis, the exact opposite has taken place.

We've now seen global debt balloon by an additional $57 trillion since 2007, raising the world's debt-to-GDP ratio by 17%. In other words, we're now more overleveraged than before the crisis.

Not surprisingly, a large portion of government debt growth originated specifically because of the crisis. New taxpayer guaranteed debt was used to repay or otherwise secure delinquent or trash debt.

And yet when used properly, debt is a solid, proven financing option to fund crucial projects like infrastructure expansion, acquire income-producing properties, and facilitate homeownership. In excess, the servicing costs of too much debt slows growth and ups the risk of future financial crises and exacerbates their accompanying fallout.

McKinsey's Debt and (Not Much) Deleveraging report examines the state of debt across 47 nations - 22 advanced and 25 developing.

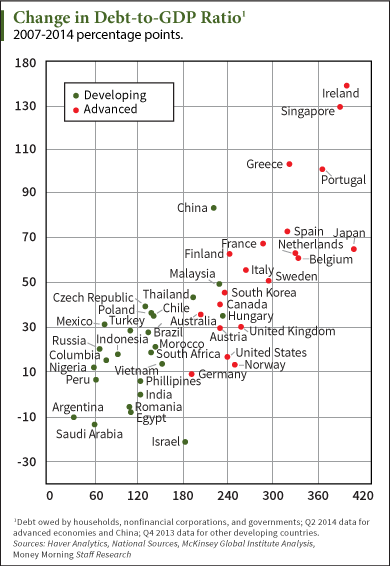

Overleveraged real estate financing is a problem reaching well beyond China. The study finds that mortgages are the main source of household debt in advanced economies. Low rates - thanks in part to the Fed and its ZIRP - have spurred larger mortgages, leading in turn to house prices being bid ever higher.

Debt-to-income, debt service ratios, and price changes point to seven troublesome economies. McKinsey says the Netherlands, South Korea, Canada, Sweden, Australia, Malaysia, and Thailand are at highest risk.

So does the consulting firm offer any concrete solutions to these problems?

Sadly, no. Instead, the Institute spews out all-purpose solutions to government debt like more widespread asset sales, one-time taxes on wealth (which I've warned you about before), and more effective debt-restructuring programs.

Given the dire state of government and household debt, what can you do to improve your own situation and avoid becoming a victim of leverage?

[epom key="ddec3ef33420ef7c9964a4695c349764" redirect="" sourceid="" imported="false"]

Also, if things sour and we face high inflation or even hyperinflation in the future, your debt will at least be partially offset and inflated away. That's because you'll have the benefit of paying back an old debt with new dollars that are worth much less, putting you in a favorable position.

Like I said at the outset, debt can be a great tool if employed properly and in moderation. Use it improperly, and the results will deeply undermine your financial stability. But if used temperately, you can benefit while limiting downside risk.

{kind=link}

{kind=link}