There are many indications that the euro is preparing for a fall, but don't short the euro just yet.

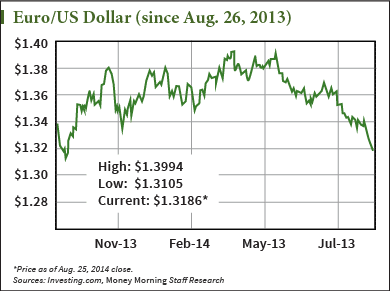

Since hitting a 2014 peak on May 6 of $1.3929, the euro has lost close to $0.08 against the dollar, or 5.4% as of Tuesday's close. At $1.317, the euro is trading at its lowest levels since September 2013.

Now there are a handful of economic factors taking place in Europe that all point to a lower euro value.

But before you try to profit off the weakening currency, it would be wise to wait for the market to kick out some of the bears. The currency is likely to rise in the short-term before starting its long-term slump.

Here's why - but first, a look at what's driving the euro lower...

Finding the Right Time to Short the Euro

The economic factors are ripe for European Central Bank President Mario Draghi to begin a widespread sovereign bond-buying spree across the whole of Europe, thus fueling inflationary pressures and pulling down the value of the euro.

Inflation in the Eurozone dropped to a four-and-a-half-year low of 0.4% in July and unemployment is at 11.5%, according to Eurostat, and quantitative easing is becoming inevitable.

"This is pretty much set in stone; it's a question of 'when' at this point and no longer 'if,'" said Money Morning Resource Specialist Peter Krauth said.

The weakening of the euro would not just be a symptom of large-scale euro stimulus, it would be a direct goal of policymakers. The financially weaker periphery countries of the Eurozone, such as Portugal, Ireland, Greece, and Spain, whose current account deficits helped to precipitate and inflame the financial crisis in Europe, would love to see the euro weaken to bolster exports.

But the ECB is only in control of monetary policy levers, and for the Eurozone to properly fight the looming threat of deflation - and for a substantial devaluation of the euro to take place - the member countries are going to need to coordinate more closely on a fiscal policy.

"Unlike in other major advanced economies, our fiscal stance is not based on a single budget voted for by a single parliament, but on the aggregation of eighteen national budgets and the EU budget," Draghi said at the economic symposium last week in Jackson Hole, Wyoming. "Stronger coordination among the different national fiscal stances should in principle allow us to achieve a more growth-friendly overall fiscal stance for the euro area."

And there are signs that this coordination is starting to take place...

Signs of New Eurozone Policy Ahead

The most recent evidence that the euro is posturing for a dive long-term comes out of France, with political infighting over the efficacy of the country's austerity measures since the 2008 financial crisis prompting the resignation of Prime Minister Manuel Valls' government (Monday).

This resignation serves to more visibly frame the discontent that French officials have for the austerity policies of President François Hollande, most eloquently articulated by Economy Minister Arnaud Montebourg.

"The priority must be exiting crisis and the dogmatic reduction of deficits should come second," Montebourg told the French newspaper Le Monde in an interview.

France is the second-largest economy in the European Union (EU) after Germany, and with its deficit doves trumpeting a louder call for stimulus, it could prompt France to slowly abandon the path of austerity that has been well-trodden by the region's standard bearer, Germany.

France doesn't want to alienate Germany and is mindful of the relationship, but senior economist at Moody's Analytics, Tu Packard, told Money Morning, "they don't want to slit their throats" by pursuing a policy they perceive as an ineffective response to their economic woes.

If France departs from austerity, it will add to a growing chorus of European officials and economists calling for more hands-on action from the ECB and widespread fiscal cohesion of the euro's members.

This would pressure German Chancellor Angela Merkel to walk back her strict adherence to the school of austerity and listen to the voices in her own country calling for a more stimulative approach.

"Germany is not speaking with a single voice," Packard said. "There are a lot of people in Germany that think they should do more to stimulate the European economy and Germany has a lot more fiscal space to do this."

If the Germans, the typical austerity stalwarts, budge on a more stimulative fiscal policy prompted by louder support from the French, the currency could begin to devalue in the longer picture.

That's when the euro becomes a short candidate.

Before then, don't be surprised if there's a short-term rise...

When to Short the Euro

With the euro trading below both its 50- and 200-day moving averages for close to two months now, it could flatten out, and even experience gains, in the short-term.

"I wouldn't be jumping to short the euro right now," said Krauth. "I do believe we might actually get a little bit of sideways action and a little bit of a climb at this point just because we've had a clear and extended drop."

The euro has been trending downward since its May high, and Krauth said it will only be so long before it reverses at least some of these losses and shakes out a few of the euro bears.

Another reason for a short-term climb is that when it becomes clear the ECB will begin its all but inevitable money printing stimulus for the Eurozone, that slight blip of perceived certainty for Europe will help drive the euro higher.

Though once that enthusiasm subsides, the euro will respond more appropriately to inflationary factors inherent upon widespread monetary easing and fall. Any slight bounce in the euro's value won't stay too long.

"I don't believe that it's done falling," Krauth said. "It will fall considerably."

If you want to get in at the right time, Krauth said to wait for the euro to touch back on its support levels of about $1.33 to $1.34, where it was trading earlier in the month.

Krauth also suggests getting in on the ProShares UltraShort Euro ETF (NYSE Arca: EUO), an exchange-traded fund that aims to generate twice the inverse daily returns of the dollar price of the euro.

More on profiting from Europe: Economic skirmishes like the situation in Russia can quickly escalate into all-out trade wars, where even the victors lose. But you don't have to be another victim. Here's how you can understand, and profit from, this surging European volatility...