Postcards from the florida republic

An independent and profitable state of mind.

I give away these Momentum readings for free every day.

These are the ultimate equalizer for retail investors against big, greedy institutions.

No guessing. No silliness. No chasing headlines from journalism majors who don’t understand finance.

When momentum goes RED, it aligns with the START of major net outflows in equity markets (read: there’s MORE HEAVY selling than buying). Could last a day… could last two months…

The reading also suggests that a major liquidity event is happening in major economies.

Best of all, it indicates that a very important pattern of behavior is on our radar — and a very profitable one.

Today – I’ll let you in on this secret.

Then, you’ll see the exact chart telling you when to load up on equities.

Listen up.

We’ve Seen This Before… A LOT.

The last time momentum went red across the board (all three readings) was March 7 - just before the Regional Banking crisis.

The markets sold off, we largely moved to cash, and we waited to reenter new positions.

After Silicon Valley Bank collapsed – the Federal Reserve bailed out the banks swapped capital for long-duration bonds to its member banks. This shored up the financial sector (for now).

After this bailout policy direction… a subset of “in-the-know” investors piled into their “favorite” stocks.

Those stocks then took off like a rocket.

The same pattern happened during a crisis in September 2022.

Red momentum, then a major global event (England’s Gilt Crisis), a policy reaction from central banks, and then the same activity among the same group of investors.

It also happened in June 2022. And March 2020. And December 2018. And August 2011. And March 2009. And October 2008.

Again… each time… four steps.

1) Big adverse market event…

2) Big move by policymakers.

3) Big buying by the same group of investors.

4) The markets rebounded – and these investors got rich.

There is ONE more VERY important month that I didn’t mention…

It might be the most important today.

It aligns with why markets have sold off in the last two weeks.

What Causes Such Outflows?

I’ll admit: When momentum turns red and outflows accelerate, no one tends to know right away why it has happened.

The selling took us negative on March 7. But we’d been in a choppy sideways market since a top on February 2, which accompanied an early signal to start taking gains.

We didn’t know why it went negative until a week later:

The regional banking crisis.

Do a Google News search for “regional banks” on and before March 7, 2023.

You won’t find much mention of regional banking problems.

The following week – however – you couldn’t shake the story.

Every financial publication wrote about it, setting off a panic in regional banking stocks.

We got out of the way… a week prior. From March 7 to March 24, the SPDR S&P Regional Banking ETF (KRE) fell more than 30%. At that point, those buyers loaded up on their favorite stocks.

The same pattern happened on June 8 of last year.

Our reading turned Red, and suddenly the market collapsed.

We wouldn’t know until a week later that it was the largest hedge fund selloff in 15 years.

The S&P 500 fell about 12% in nine days.

Sometimes the situation was more obvious.

When this went red on February 21, 2020, and we sold many equities, it was COVID.

The market would crash by 33% not long after it went red.

We’d buy back – based on the reading – on April 6, 2023. Of course, that curious subset of investors was also buying BIG.

And they made a killing while most people were afraid to buy.

That should capture your attention.

Who the heck are these people?

Why Is Momentum Red Now?

Before we get to them, let’s discuss recent events.

This week’s negative turn has been a bit more questionable…

As I’ve noted, there are many negative stories in the markets.

Japan’s Yield Curve Control could spell trouble for U.S. bonds. In the U.S., inflation is running hot again. In addition, the Treasury Department is facing problems as it needs to get investors to buy long-term bonds and not load up on short-term debt that needs to be rolled over in two years.

And then, there is the recent downgrade by Moody’s of one-seventh of the American banking system.

Bond markets tell us that the Fed isn’t done hiking, that inflation is likely heading higher, and that the Treasury Department faces problems getting people into long-term bonds.

But the other BIG problem we’ve highlighted here is China.

On June 1, China’s central bank eased – helping propel an undeniable market rally.

The same thing happened in January this year. See the yellow boxes for moves on the S&P 500 SPDR ETF (SPY).

But in mid-July –when a U.S. Senator hedged his portfolio against the Nasdaq 100 – China tightened by more than what they had eased in June.

The nation was trying to provide support for its currency.

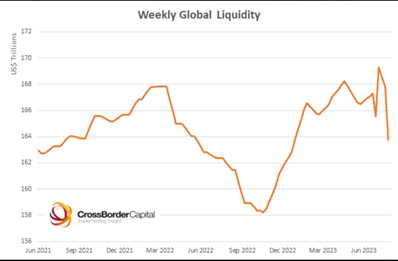

That’s how you end up with a big drop in global liquidity – as referenced by CrossBorder Capital in this recent chart. Behind this paywall, authors point to a sizeable reduction in their Global Liquidity Index from June to July.

China is facing renewed problems.

The financial press is starting to pay attention.

Stories are trickling out from this notoriously censorious nation. They show two serious issues.

First, China’s Consumer Price Index (CPI) came in at NEGATIVE 0.3% for July. Bloomberg noted Friday that deflation is now the nation’s greater market risk. That was Friday.

Second, there’s a big problem in China’s real estate market.

The Wall Street Journal noted August 5 the following:

Shares and bonds of property giant Country Garden Holdings dollar-denominated bonds maturing in January 2024 are trading at 25% of their notional value, compared with 81% as recently as mid-June.

This is a big deal.

We’re now two years past a huge debacle involving China’s property giant Evergrande. And… eight years after another crisis nearly tore down the nation’s economy.

On Thursday, Mike Shedlock (FREE required reading) noted again that China has a serious demographic issue that will weigh on them. The nation has been trying to achieve rapid growth – and the only way to do so has been through massive government spending and debt. The entire situation is very similar to Japan’s long-deflationary challenges.

Now – here’s the thing. China’s problems can and will weigh on global equity markets. And China has two choices – pretty much the same choices that all major central banks have today.

Because they are so debt-heavy, China can allow assets to crash.

Yet, the Chinese Communist Party (CCP) risks having the nation’s real estate market take them down with it (talk about a Black Swan event).

Or – the People’s Bank of China (PBOC) can “print” more money.

After all, this is the way that central banks try to tackle deflation by easing policy.

Yeah!

Maintain power and keep pumping asset prices higher and higher so that they end up pricing out the youngest members of society from owning real assets like housing.

Do those two things sound familiar?

They should. Both are happening in the United States as the same cabal that created the problems for 30 years cling to power.

How to Address China

Momentum is negative.

We’re mainly sitting in cash over in the Republic.

We’re going to the northern beaches.

We’re floating around in the backyard pool.

This could get rocky over the next few weeks.

But I anticipate that China’s central bank will return to its usual ways – providing more support to its economy and keeping the shell game running.

We want to see two things happen.

First, we’ll pay close attention to the policy response from the PBOC. That response, however, might not be immediate.

It could require another trip to Beijing for Janet Yellen – or broader questions about China’s plan for the BRICS currency.

Could, for example, China work with Saudi Arabia to provide some support for its currency?

I’m not a Chinese policy expert, though.

So, I don’t care what they do… just that something’s done.

I’m watching the news feed and waiting for a positive response from the Direxion Daily FTSE China Bull 3X Shares ETF (YINN). More on that ETF this week, but it will provide clues that something happened, and we are on the verge of rebounding.

Second, if things get nasty for the global markets, we want to monitor that specific subset of investors that BUY when we see major policy changes.

Those investors are corporate insiders (CEOs, CFOs, 10% owners, board directors, and Chairpersons) at S&P 500 companies.

How to Address U.S. Markets

Look at this chart.

This is the insider buying-to-selling ratio of S&P 500 stocks.

It shows the actions of executives buying their stock in periods of turmoil.

When that insider buying ratio is HEAVILY tilted to the buyers, it signals they are collectively calling a bottom on the market.

When the BLUE LINE is at the top and moves higher – it’s time to buy, even if it’s just for a few weeks or months.

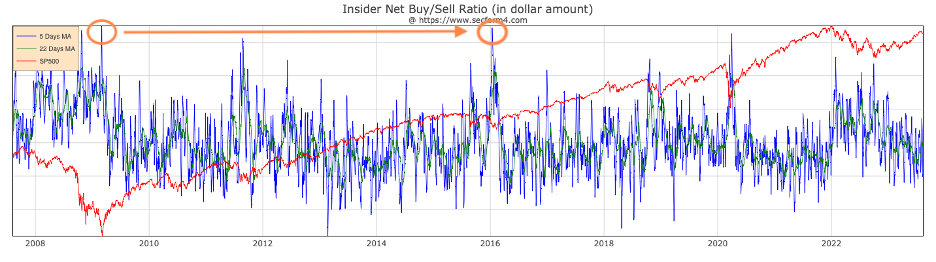

Look at January 2016.

That was the marked end of the Chinese market turbulence period that had lasted months.

In January 2016, central banks around the globe announced intentions to keep interest rates low in response to weak Chinese growth. The markets had just experienced about a 14% drop from mid-December 2015 to the lows of January 2016.

After markets cratered that month, central banks accommodated policy changes… including actions from the PBOC and the Bank of England.

Well, wouldn’t you know it?

Corporate insiders loaded up on stocks faster since the start of the Fed’s Quantitative Easing in March 2009. It’s RIGHT THERE.

After that HUGE round of insider buying, the S&P 500 gained more than 16% from the bottom of January 2016 until September 2016.

Well-timed buying, indeed.

But look at the other periods on this chart.

You’ll see – again – periods of turmoil, followed by a policy response and heavy amounts of insider buying.

This Isn’t a One Time Pattern

October 2008

- Event: Lehman Brothers collapsed, creating a global credit crisis.

- Policy Response: The U.S. government authorized its first bailout plans.

- Insiders: loaded up on their stock.

March 2009

- Event: Global credit crisis accelerates.

- Response: The Federal Reserve announced its first Quantitative Easing (QE) program that injected a massive amount of capital into the system.

- Insiders: Doubled down off the October period.

August 2011 —

- Event: Black Monday, a major market downturn after a downgrade to the U.S. credit system by S&P Global due to the U.S. debt ceiling crisis. Followed QE2 period.

- Policy Response: Debt ceiling raised. European bailouts.

- Insiders: Loaded up.

December 2018 —

- Event: Bond markets panicked in October, with a frenzy spilling into the final weeks. The S&P 500 lost 20% in a month.

- Policy Response: Federal Reserve pivoted, cut interest rates, and began increasing its balance sheet.

- Insiders: Loaded up.

March 2020

- Event: COVID lockdowns.

- Policy Response: U.S. created 1/3 of all dollars in existence—massive Congressional stimulus.

- Insiders: Loaded up on their stock.

January 2022

- Event: After the selloff from November 2021.

- Policy Response: Fed and Treasury Department attempted to argue that inflation was transitory. It wasn’t.

- Insiders: Loaded up that month. S&P 500 rebounded 7% despite chopping into April.

October 2022

- Event: Rising interest rates hammer central banks around the world. Markets elicit concerns about England’s GILT.

- Policy Response: Over the next few weeks, we saw large policy changes from the Bank of England, the U.S. Federal Reserve, the People’s Bank of China, and the Bank of Japan.

- Insiders: Bought the bottom, doubling down on January purchases. This coincided with the lows of the last two years in terms of global liquidity.

Why We Watch the Insiders

There are no guarantees that this market will crater in the weeks ahead – but this is a seasonal period of weakness. The last thing I want is for retail investors to start panicking… without understanding how policy impacts markets…

There remain many questions about inflation, Fed policy, and more. And as far as I’m concerned – there may be another major factor in the markets that is driving this negative momentum – and it just hasn’t hit the news cycle yet.

But we can take away one important factor from these periods of volatility and uncertainty.

If there is a deep selloff and changes in central bank policy to soften the blow, the insiders will tell us when to buy.

If we see a BIG spike in the coming weeks in buying – to complement a central bank pivot – we will start buying too.

Until then, hit the beach, have a drink, and maybe get away from your computer. There’s more to life than this stuff.

That’s why we aim to keep it simple in the Republic.

Stay positive,

Garrett Baldwin

About the Author

Garrett Baldwin is a globally recognized research economist, financial writer, consultant, and political risk analyst with decades of trading experience and degrees in economics, cybersecurity, and business from Johns Hopkins, Purdue, Indiana University, and Northwestern.