By D.R. Barton

Dear Red Alert Reader,

Sitting back and assuming that Social Security is going to give you what you’ve earned is no longer a viable option.

A few years back, a Time magazine investigation determined that a married couple retiring after both spouses earned average income will receive $42,000 less in Social Security payments than they contributed to the system in taxes.

In a separate study, Social Security Advisors, a high-end consultancy firm in Manhattan, found that 71% of married couples are missing out on an average of $120,000.

Their clients were owed this money from Social Security, but for any number of reasons, they were never able to collect on it.

The only way to stop this is to take matters into your own hands. And we’re going to help you.

That’s why we’ve created this report, revealing a collection of Social Security so lucrative they could grow your net worth by seven figures.

Social Security Benefit No. 1:

Figure Out Your Life Expectancy and Get Tens of Thousands in Extra Income

It’s official – the mid-60s is the new middle age. So says a new study conducted by researchers at Stony Brook University and the International Institute for Applied Analysis. Considering this, do you really need to start collecting “old age insurance” (a time-worn moniker for Social Security benefits) when you reach your Full Retirement Age (FRA)? There’s an easy way to find out – and, most likely, chances are good that you don’t.

According to the 2015 study published in the medical journal PLOS One, age should be measured by time left to live rather than time lived. And at the current FRA of 66 for those born between 1943 and 1954 and an FRA of 67 for those born after 1960, we have a whole lot more living to do.

Here’s why…

In 1983, legislation was passed under President Ronald Reagan to amend the Social Security Act. It raised the full retirement age above 65 for anyone born in 1938 and thereafter. The act was an effort to help strengthen Social Security’s trough at a time when the program was facing imminent financial crisis.

The legislation mandates that Full Retirement Age (FRA) increase incrementally for those born between 1938 and 1943, when FRA begins at 66. Age 66 is now the magic number for those born between 1943 and 1954. After that, it increases incrementally until the birth year of 1960, where FRA peaks and ends at 67.

When figuring out your FRA, revert to the previous year if you were born on January 1. If you were born on the first of the month, figure your FRA as if your birthday was in the previous month.

For decades, arguments have persisted that this measure was not strong enough to keep Social Security afloat. Currently, there is a contentious political debate over raising the FRA to 70 or even 73. It’s a political hot potato that undoubtedly isn’t going to come to a head any time soon.

The conventional view that faster increases in human life expectancy lead to faster population aging no longer holds water because it is based on the assumption that people become old at a fixed chronological age – like 65, says demographer Sergei Scherbor, lead authority on the study. “A preferable alternative is to base measures of aging on people’s time left to death,” he says, “because this is more closely related to the characteristics that are associated with old age.”

In other words, “old” hardly fits a vibrant and active 65-year-old. Old age doesn’t really apply until you actually feel it settling in, like when you start to shuffle instead of walk or when your accrued chronic illnesses are more than you can count on one hand. In 1935, the year Social Security was launched, life expectancy was 61.7 years, so making it to 65 was almost like living on borrowed time. Getting Social Security was like a bonus!

A lot has changed in the last eight-plus decades. Currently, the average life expectancy for Americans is 78.7 (76.2 for men and 81.1 for women), but that’s just an average – hardly the maximum. How long you will actually live has to do with how the health of your body and mind measure up over time, says Scherbor. And it’s not unusual anymore to see people live vibrantly well into their 80s and even their 90s.

But what about you? You can get a really good idea of your own life expectancy by using the quick and easy tool developed by the Wharton School of the University of Pennsylvania. It takes into account your quality of living, your lifestyle, the number of health problems and health risks you’ve accumulated over the years, family history, plus other variables. You can access it by clicking this link. It shouldn’t take you more than 15 minutes to complete. And it’s something everybody should do, if you want to get your best return on all the money you’ve paid in Federal Insurance Contribution Act (FICA) taxes throughout your working life.

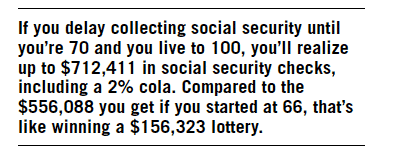

With that information in hand, you’ll get a solid idea if you’re better off collecting at FRA (or even sooner), or if you should delay to age 70, the maximum age to which you would ever want to delay collecting. The difference in waiting can mean an extra $1,649 a month, or $19,788 a year, in your pocket over the long haul if you wait – and that’s just for starters. Yet, only 1.4% of people currently on Social Security have opted for this windfall, which is sometimes called the Delayed Retirement Credit (DRC).

Whether or not it’s to your advantage to wait depends on your life expectancy compared to the age you’ll be when you reach what Social Security calls “the break-even age” – the crossover point at which you’ll move ahead of the game. If you’re like most people, you’ll be in your early 80s by the time you reach the break-even point. If chances are good that you’ll make it to this age, then it might be a wise move to wait to collect until you’re 70, especially if you’re not planning to retire at 66.

There are several sites on the internet where you can get your break- even point at a glance, but we consider AARP’s calculator to be the best free one. You can find it at: www.aarp.org/work/social-security/social- security-benefits-calculator.html. If you’re widowed, divorced, or have a big age gap with your spouse, this paid tool might serve you better: maximizemysocialsecurity.com. You’ll easily recoup the $40 license fee the first month you start collecting benefits. That’s 100% worth it in our book! Compare your break-even point age to the age you came up with on your life expectancy calculation and you have your answer.

As we said, this is just for starters. There are many more ways to get even more money out of Social Security, even if you don’t wait until age 70, and even if you take the earliest possible retirement dollars at age 62.

Social Security Benefit No. 2:

Collect $10,224 More a Year Than the Average Joe

There’s a lucrative advantage to delaying the start of collecting Social Security benefits to age 70. You’ll get 8% more for each year you delay. If your FRA is 66, that comes to 32% more in benefits, and 24% more if your FRA is 67. When was the last time you received an 8% raise from your employer? And for four years in a row to boot!

Problem is, most people don’t think this way. According to Social Security statistics, three out of four people start collecting benefits before they reach FRA and nearly half of them start collecting at the early retirement eligibility age of 62, which penalizes you by roughly 6.25% per year.

So who benefits most if you wait – you or the U.S. Treasury? Well, it all depends on how long you’re going to live beyond your so-called break-even or crossover point. Here’s an example of how it works and what it could mean to you in real dollars and cents…

Let’s say Jim and Bob are about to reach their full retirement age of 66 and are each eligible for the maximum payout of $2,658. The amount a person is entitled to at FRA is called the Primary Insurance Amount (PIA). They are entitled to the payment whether they continue working or not, though neither of them plans to retire so young.

Jim sees it as nothing but a windfall and starts collecting his $2,658 a month in full benefits as soon as he’s eligible. Bob’s thinking is more frugal and he decides to wait until he turns 70. By waiting and with all else being equal, Bob will get monthly benefits of $3,508 in today’s money. (This figure does not consider future cost-of-living adjustments that Social Security typically kicks in annually – but not always! – of around 2%.). That’s $851 a month or $10,212 a year more than Jim. Based on the same scenario, people eligible for full retirement at age 67 who wait until age 70 will put an extra $7,644 a year in today’s dollars in their pocket.

But wait just a minute. For four whole years Jim will be getting $2,658 a month from the government while Bob gets zip. Added up, that’s $127,584 – a mortgage payoff maybe, or a college tuition or, what the heck, maybe even a brand new Tesla. If Jim had started taking benefits at 62, he would only collect $1,993 a month, but he’d get an even bigger head start on Bob – by $191,328. Heck, that kind of money could buy him a Bentley!

So, who’s better off?

Of course, no one knows when they’re going to die, but actuaries and any array of Internet-based life expectancy tools like the one we suggested can give you a pretty good idea. Compare your life expectancy to your break-even point (see above how to calculate this) and let that be your guide. Knowing your break-even point is must-have information you need to make your decision.

For a lot of people like Bob, it pays to wait. The extra $851 a month he’ll receive by waiting means he’d have to live another 12.5 years before he breaks even. After that, Bob will move ahead of people like Jim by leaps and bounds year after year.

That might sound like a long-range gamble, but consider that Bob would still only be 82.5. And keep in mind that just as many American men live beyond age 76.2 as die before. Is it worth it to you? Let your health, lifestyle, and actuary be your guide.

Social Security Benefit No. 3:

Add $1,269 to Your Social Security Bottom Line – and More With Each Passing Year

If you’re old enough to be eligible for Social Security, you can remember back to 1980, a time of sky-high interest rates – and for those fortunate enough, handsome salary increases. Even Social Security in that year gave its “seniors” an unheard of 14.3% increase, something that hadn’t been seen before and has never been seen since.

In 1975 the federal government passed legislation establishing increases in Social Security based on a formula tied to the Consumer Price Index for Urban Wage Earners and Clerical Workers. The feds call it a Cost of Living Adjustment, or for short, COLA. Since then, Social Security recipients have received an increase every year except for in 2009, 2010 and, as was recently decided, 2016. Over the years, increases have ranged from a low of 1.3% in 1998 to the already mentioned

14% or more in 1980. In 2014, the increase was near an all-time low at 1.7%, a number it’s been hovering at for the last few years. In fact, the last meaningful increase was in 2008, when COLA came out at 5.8%. However, historically, the average increase is 3.98%. And that’s where this little-known secret comes in.

Just shy of 4% doesn’t sound like much of a raise – until we go back to the decisions Jim and Bob made concerning the timing of their Social Security and that decision the feds made in 1975. When you multiply Bob’s $3,508 by 3.98% and again by 12 months, his income jumps by $1,675 a year versus the $1,269 a year Jim is going to get. That’s a difference of only $406, you might say. In five years, however, Bob’s Social Security insurance will go up by $9,070 a year compared to Jim’s $6,873 — a $2,198 difference. And it will grow exponentially over time, almost like compound interest. This is another reason why the Social Security system loses when you postpone your entitlement – and why they don’t rush to tell you about it when you go to sign up. The earlier you start collecting, the less it’s going to cost the government over the long haul.

Social Security Benefit No. 4:

Receive an Extra $127,296 – if You’re an Unmarried Couple

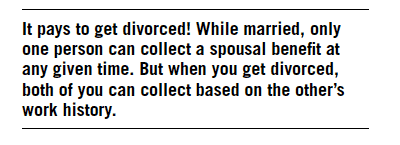

Believe it or not, the federal government provides you an incentive to get divorced and live, as they say, “in sin”. If you were married for at least 10 years and then divorced for at least two years, you can collect what is known as Divorced Spouse’s Benefits, in which the lower-paid ex-spouse is entitled to the higher of two options: The Primary Insurance Amount based on the deceased’s earnings, or half the amount the surviving spouse is entitled to collect.

It’s a boon for the lower-paid spouse because it gives her or him the opportunity to let their PIA grow by approximately 8% a year, with the potential to switch over to a larger benefit at or before age 70. Prior to new legislation passed in November of 2015, you were allowed to choose which way you wanted to go. The catch here is that Social Security only allows one person to collect spousal benefits. But it still stands that if you untie the knot at least two years before you qualify for full retirement benefits, you can both get free Divorced Spouse’s Benefits.

Granted, you’re gaming the system with this strategy, but two happily married people can decide to get divorced and live together “in sin” so both can collect spousal benefits off the other and delay collecting full benefits until age 70. Spousal benefits of 50% generally equals one full retirement benefit for the two of them until the older reaches 70.

The difference can bank you as much as $60,000 in free spousal benefits. Once you’re both 70, you can each claim an even higher personal benefit, remarry, and live even happier ever after.

Social Security Benefit No. 5:

Delay Divorce to Your Financial Advantage

It used to be that 50% of marriages ended in divorce, but that appears to be declining, mostly due to people putting off marriage until they’re a little older and a lot smarter. Still, 20% of marriages dissolve within the first five years, and it rises to 33% by 10 years.

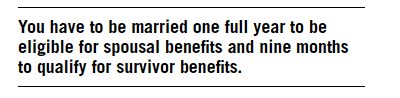

With that in mind, here’s important need-to-know information, whether you’ve been (or will be) married once, twice, or even more. Do whatever is necessary to make it to the 10-year anniversary – especially if there is a disparity in your incomes. It will mean thousands of dollars in your pocket over and above what you’ll end up settling for in divorce. However, you only qualify for a spousal benefit if you were married for at least 10 years, you’ve been divorced for at least two years, and you have not remarried.

Now, here’s the sneaky secret: The only requirement is that you be married. You don’t have to be living together – the Social Security system doesn’t care about that. Get legally separated if you want. Social Security doesn’t care about that either. All it cares about when it comes to doling out an ex’s benefits is that the marriage lasted 10 full years. Even if you file for divorce and it is granted one day after your tenth anniversary, you’re golden.

If you must, move out of the bedroom, or take a wing of the house for your own, or move home with mom or in with a buddy, or get your own apartment. Do whatever you have to do to make life livable. Just don’t get divorced – at least not yet. Remember, when the going gets tough, just take a deep breath and count to the magic number ten.

Social Security Benefit No. 6:

Supercharge Your Survivor Benefit

It’s pretty much common knowledge that when the higher-income earner in a marriage dies, the larger Social Security benefit reverts to the lower-income spouse. But wait – don’t be so fast to file for that survivor benefit.

The whole idea of survivor benefits harkens back to the days when most women were homemakers and didn’t hold full-time jobs for enough years to matter much in terms of Social Security income. Times have changed and there’s more to survivor benefits than “tradition.” There are little-known strategies worth thousands of extra dollars to widows and widowers who are eligible for benefits based on their own work records.

Why? Because you have both the survivor’s benefit and your own worker’s benefit on which to build your Social Security retirement strategy. Most people don’t realize this and assume they are entitled to a survivor benefit or their own worker benefit, so they file for the higher of the two. Avoid falling into this trap, which Time magazine called “one of the trickiest filing rules.”

There are no spousal benefit opportunities if a marriage ends in the death of one partner. That’s actually good because where a spousal benefit is worth 50%, a survivor benefit is potentially 100%. Also, you become eligible for a survivor’s benefit at age 60, however opting for it at any time before Full Retirement Age means that your benefits will be permanently reduced. This might sound like a good idea when you consider that a spouse might have left behind a full retirement benefit of $2,658 a month. And even at the reduced rate of $2,152 a month taken at 62, it may still be more than what the survivor qualifies for on her own record. But there are ways to work the system if, like the majority of people, you have paid FICA taxes for the mandated 40 quarters.

Let’s say 67-year-old George left Elaine a widow at age 60. She could start collecting a reduced-rate survivor benefit immediately and allow her own worker benefits to grow while she continues to work. Then, at age 70 she can switch over to her own now-higher worker benefit. Alternatively, and assuming she has the means to get by, she could delay collecting the survivor benefit anytime up until she reaches 65 and 11 months. (Due to a foible in the law, people born between January 1, 1943 and December 31, 1954 attain Full Retirement Age one month earlier than everyone else.) There’s no sense to wait longer because survivor benefits do not grow beyond the survivor’s FRA.

If Elaine hadn’t accumulated the same level of benefits as George, another option would be for her to take her own worker’s benefit at age 62, then switch to her higher survivor’s benefit at full value at age 65 and 11 months.

There are other options to move benefits around even if your spouse dies after you’ve started to collect. For example, it’s possible to start taking worker benefits at age 62, step it up to spousal benefits at age 66 (or 67), and then inherit an even higher survivor benefit when the spouse dies.

Social Security Benefit No. 7:

Collect 50% More When Your Ex Dies

As with spousal benefits, survivor benefits apply to ex-husbands and ex-wives. It doesn’t matter how many exes the deceased collected during his or her lifetime. When he or she dies, you can switch from spousal benefits to survivor benefits and collect twice as much. The same rules still apply as with the spousal benefit: You must have been married at least 10 years, divorced two years, and have not remarried.

Social Security Benefit No. 8:

Give Mom a $26,304 Annual Payback

Here’s one we guarantee nobody ever thinks to ask about: a parent benefit. A parent who is at least 50% dependent on a child for support can cash in on a child’s social security should the offspring die. The parent is eligible for 82.5% of the deceased’s Primary Insurance Amount, which amounts to $2,192 a month, based on the same maximum payout of $2,658 that we’ve used in earlier examples. However, a parent can’t collect both their own Social Security and their child’s. Social Security will pay whichever is the higher of the two.

Social Security Benefit No. 9:

Get a One-Year Interest-Free Loan from Social Security

It’s budget time, and with it frequently comes the edict: Cut the budget by cutting personnel. So, the next day you go to work, open your e-mail, and find a curt message from the CEO. Your division is being downsized and your services are no longer needed. Your mind races: I’m 62. How am I going to find another job? What am I going to do for money?

Well, one thing you most certainly can do is march down to the Social Security office and sign up now, even if early retirement is not your intention. A little-known loophole called Withdrawal of Application allows you to collect Social Security for one year and then pay it back. It’s as good as getting a one-year interest-free loan from the government! Once you’ve paid it back, you’re eligible to re-sign up at a later date without penalty. It’s a sound short-term strategy for an older someone in a monetary pickle who expects to get back on his feet in the near future.

At one time, Social Security allowed anyone to repay all their benefits in order to accrue additional credits and collect a larger monthly payout at a later date. A 2010 rule change limited this loophole to a one- time, one-year offer.

Social Security Benefit No. 10:

Put Off Getting Remarried Until Age 60 to Boost Your Income

Survivor benefits are good for life, unless you decide to remarry before the age of 60. So, examine your options with scrutiny. If you remarry after the age of 60, you have the option of continuing your survivor benefits for life or switching later on to spousal or full retirement benefits. For example, let’s say your new honey has a higher income level than your dearly departed. You can continue to collect survivor benefits until the age of 66 or 67, at which time you can transfer over to spousal benefits or your own worker benefit at age 70, whichever is higher.

Social Security Benefit No. 11:

Leave Your Spouse a $30,112 Annual Legacy

Another advantage of waiting until 70 to start taking Social Security is to provide income protection for your surviving spouse. This means that if, at the time of your death, she was collecting less in Social Security than you were, you can leave her a legacy of a higher income.

For example, let’s say Mark and Carol are both the same age with a Primary Insurance Amount of $16,000 a year. Carol starts taking a reduced benefit of $12,000 (75% of her PIA at age 62). Mark delays his benefits until age 70, racking up 32% higher payments. Suppose Mark dies at age 82. Counting in a cost of living allowance of 3% for 12 years, it would give him an annual income of $30,112 in his final year. This now becomes Carol’s survivor benefit.

If they both had started collecting at the same age, however, there would be no difference in their incomes and at Mark’s death, two checks would simply be cut down to one. How many widows or widowers can realistically maintain their lifestyle when half of their income disappears overnight? This is something most couples don’t even think about. But since Mark delayed his benefits, he’s leaving a $30,112 legacy for Carol, $8,439 a year more than she was already collecting.

As in this case, many married couples may find that it’s beneficial for the lower-earning spouse to start collecting early while the breadwinner delays. When considering a strategy such as this, it’s important to consider the projected longevity of both spouses.

Social Security Benefit No. 12:

Cut Your Retirement Tax Penalty by 36%

It can be tough to live on Social Security alone. That’s why it’s called supplemental insurance. Most people have a nest egg stashed away somewhere in a tax-deferred plan, such as a 401(k) or IRA. It can add up quickly. You contribute, your employer matches your contribution, it’s all invested, and it grows for decades. But at some point, it eventually has to be withdrawn – and then taxed.

And here comes the double-edged sword. While we all realize we eventually have to pay tax on our deferred-tax plans, it can put retirees in a taxable situation much deeper than expected. Withdrawing from your 401(k) also means you’ll generate a higher income, which can then trigger higher taxation of your Social Security benefits.

The tax-free threshold on Social Security is low – $25,000 for singles and $32,000 for a married couple. After that, up to 50 cents of every Social Security dollar is taxable. At a second threshold of $34,000 for singles and $44,000 for a married couple, up to 85 cents of each dollar is taxed. This means that every dollar you withdraw from your IRA can expose 85 cents of each Social Security dollar to taxes.

Here’s a strategy even most tax accountants don’t know about. Because Social Security and your IRA are taxed differently, you can reduce your

tax penalty by choosing to maximize your Social Security income and reducing your withdrawals from tax-deferred retirement accounts. A lot of accountants make the false assumption that taxes on Social Security can’t be avoided and figure 85% of all Social Security will be taxed as ordinary income once that second threshold is crossed. Not so!

A loophole in the Combined Income Formula shows that opting to trade higher Social Security income for lower IRA withdrawals will save you tax dollars. This is because only half your Social Security income goes into the formula, while 100% of your IRA withdrawals do.

It’s just one more reason why delaying taking Social Security until age 70 works to your benefit, because you can minimize your IRA withdrawals when you get higher social security income. Every dollar you take as Social Security instead of tax-deferred income lowers the tax toll from 46.25% to 10.62%. That’s a tax savings of 77%.

In dollars and cents it means that a married couple could get $64,000 in Social Security income – counted as $32,000 in the Combined Income Formula – before they would exceed the first threshold. It means that even people with an after-tax income of less than $100,000 can save significant tax dollars by delaying Social Security.

Social Security Benefit No. 13:

Reduce the Taxes on Your Retirement Income

This is not an option for most people, but it can work for some: Convert your IRA funds into Roth IRA accounts. It eliminates the Required Minimum Distribution that kicks in at age 70 ½ on IRA savings. This means you can draw down on your tax-deferred savings at an even slower pace and avoid further taxation on your Social Security. Of course, you have to be able to afford to do so.

There’s also a benefit in this for your heirs. When you earmark Roth IRAs as a legacy bequest, your beneficiaries can then take tax-free income over their own life expectancies under a provision known as a Stretch IRA. Not all IRAs allow for this strategy – make sure to check with your personal financial advisor.

Social Security Benefit No. 14:

Get Back the Social Security Money You Left on the Table

If, after reading all this, you feel you’ve missed out on a big opportunity to optimize your Social Security, you can get back some of the money you left on the table. Social Security will give you a retroactive check for up to six months for full retirement, survivor, and spousal payments. If you missed the opportune time to file for spousal benefits, for example, Social Security will cut you a check for up to $7,972 – $1,329 being the max multiplied by six.

Social Security Benefit No. 15:

Work the System to Your Advantage

As you can see, there is a wide array of payments you can get from Social Security beyond your own worker benefit, if you know how to work the system. Your spouse, your kids, and even your parents can potentially benefit. If you become disabled, a whole new set of benefits will kick in to the advantage of you and yours. Any way you look at it, it is a very good deal – and why delaying your own benefits can provide extra income to your family during your lifetime and after you die.

But there’s a catch. Social Security calls it the Family Maximum Benefit (FMB), which puts a cap on the amount of combined benefits you can receive at any one time. It is probably the trickiest aspect of planning your Social Security strategy. The FMB limits the amount of benefits other family members can collect to 150-180% of your PIA. It doesn’t mean they can’t collect – it only means Social Security will reduce their total benefits so they do not exceed the maximum allowable. Your benefits, however, cannot be touched.

The FMB is formulated on a complicated equation based on your earnings record and generally equals 175% of your PIA. This percentage limit varies slightly based on the type of benefit you’re requesting.

Of course, there are ways around it all, but it means your family needs to be flexible. One way to stay under the ceiling is to stagger your family’s benefits. For example, if spousal and child benefits put your family’s overall Social Security income over the top, then you might want to postpone collecting spousal benefits until one child turns 18. Since both benefits are half of yours, family income will not change at all.

Social Security Benefit No. 16:

Do It All Over Again and Collect an Extra $246,240

Almost half of all Social Security recipients – a solid 45% – take benefits as soon as they can, at age 62. Many of them live to regret it. In fact, you may have your own regrets right now after reading all these different ways you can optimize your share of Social Security. You may even be wishing you could just start over again. Well, guess what – you just might be able to.

If you started to collect during the past year, you can file what is called a Withdrawal of Application, or what we call the Do-Over Strategy. It means you can pay back what you received and go back to square one. This strategy is so little known that only 71 people took advantage of it in one recent year. Yet, the payoff can be really big.

Let’s say you’re now getting $1,500 a month in benefits. If you pay back the money you’ve collected within the first year, which is just $18,000, and delay until the age of 70, your benefit will grow to $2,640. Now, $18,000 may sound like a big chunk of change, but at the end of a typical 17-year retirement you’ll have put an extra $232,560 in your pocket – and that’s not even including cost of living increases.

But you could get even more. That’s because this $232,560 bonus is based on a modest PIA at age 66 of $2,000. If you have the maximum PIA of $2,686, you’ll end up with an additional $312,314. That’s why we call this strategy the $312K Secret.”

If this option is available to you, it’s something you should seriously consider. This do-over strategy applies to all benefits.